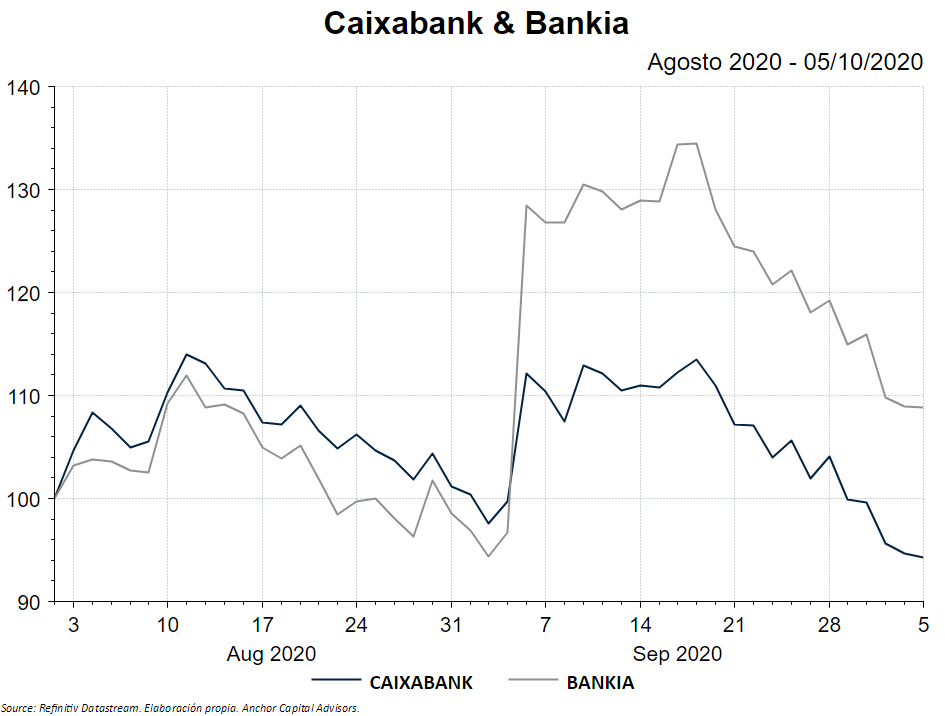

The takeover of Bankia by Caixabank has occupied a large part of the economic headlines during the month of September. It makes sense, since it is the largest operation between two Spanish companies in history.

It seems that times are changing in the spanish banking industry. After this takeover, there are also rumors of a merger between Liberbank and Unicaja.

When the rumors of a merger between CaixaBank and Bankia were announced, optimism on the stock market was unleashed. As expected, the shares of the absorbed company, in this case, Bankia, soared.

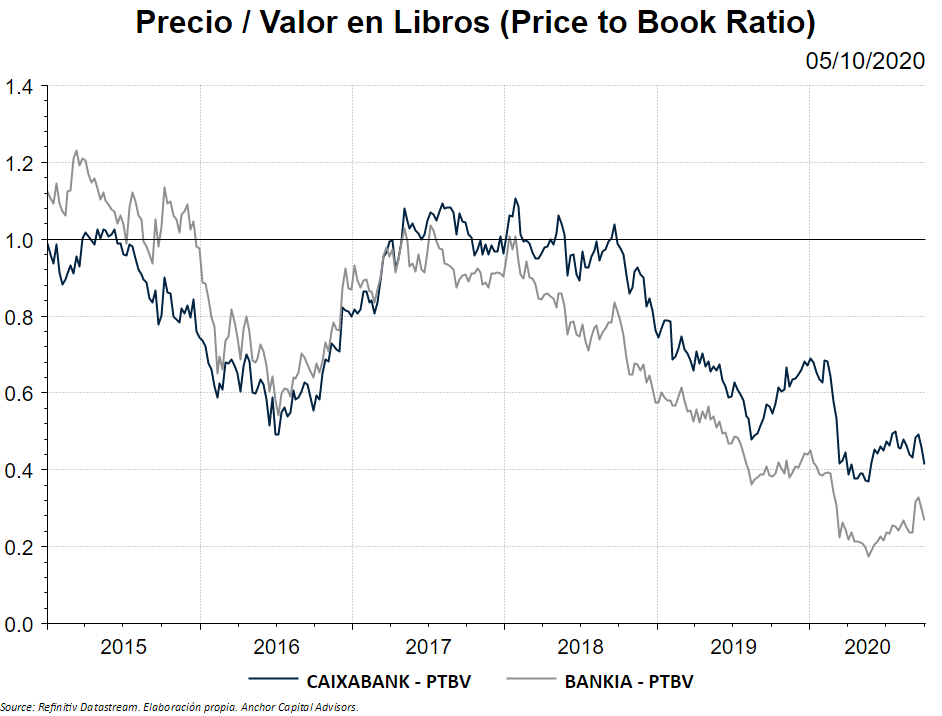

As we already mentioned in the post What is happening to the Banks?, European banks are very affected in terms of profitability.

Because they have a large volume of assets and the rates are very low, the return on total assets (ROA) is very low.

Similarly, as banks' capital requirements are increasing, the return on their equity is lower (ROE). They are not allowed to issue debt above certain levels and thus increase their profitability with leverage. This is where the binomial between solvency and profitability appears. These low returns are priced in the market.

Because they have a large volume of assets and the rates are very low, the return on total assets (ROA) is very low.

Similarly, as banks' capital requirements are increasing, the return on their equity is lower (ROE). They are not allowed to issue debt above certain levels and thus increase their profitability with leverage. This is where the binomial between solvency and profitability appears. These low returns are priced in the market.

Giving the absence of business profitability, the search for greater productivity, greater efficiency in processes and generation of synergies may be one of the reasons why these entities merge.

On the other hand, bank concentration will be one of the topics of debate in the upcoming years. Although Fintech companies are taking part of the pie, they have little capacity to give real credit to the economy. Here, the big banks, with its enormous distribution network and resources, are the winners.

However, economies of scale are put aside when all the banking business depends on one variable: the European Central Bank. The 2008 financial crisis and the Euro crisis in 2012 harmed so much the banking sector, triggering the authorities (led by the ECB) to increase control over banking.

And it is that perhaps, in the socialized Europe of the XXI century, we will go towards a single public bank: the ECB. In this way, the big banks would be replaced by mere branches of the Central Bank, thus making the banking model in Europe, which lacks innovation, to be at the orders of the central bankers.

Perhaps this is the underlying reason why bank concentration is increasing. Despite the fact that there are many banks in the market, the product is so homogeneous and controlled from above that there is little room for differentiation.

If we make the comparison with a symphony orchestra, it is clear that the ECB would be the director. In addition, we would see how the orchestra does not welcome soloists or virtuous musicians, the instruments would be of the same type, all string, wind or percussion, and they would all play the same chord. An uncomfortable experience, in short.

On the other hand, bank concentration will be one of the topics of debate in the upcoming years. Although Fintech companies are taking part of the pie, they have little capacity to give real credit to the economy. Here, the big banks, with its enormous distribution network and resources, are the winners.

However, economies of scale are put aside when all the banking business depends on one variable: the European Central Bank. The 2008 financial crisis and the Euro crisis in 2012 harmed so much the banking sector, triggering the authorities (led by the ECB) to increase control over banking.

And it is that perhaps, in the socialized Europe of the XXI century, we will go towards a single public bank: the ECB. In this way, the big banks would be replaced by mere branches of the Central Bank, thus making the banking model in Europe, which lacks innovation, to be at the orders of the central bankers.

Perhaps this is the underlying reason why bank concentration is increasing. Despite the fact that there are many banks in the market, the product is so homogeneous and controlled from above that there is little room for differentiation.

If we make the comparison with a symphony orchestra, it is clear that the ECB would be the director. In addition, we would see how the orchestra does not welcome soloists or virtuous musicians, the instruments would be of the same type, all string, wind or percussion, and they would all play the same chord. An uncomfortable experience, in short.