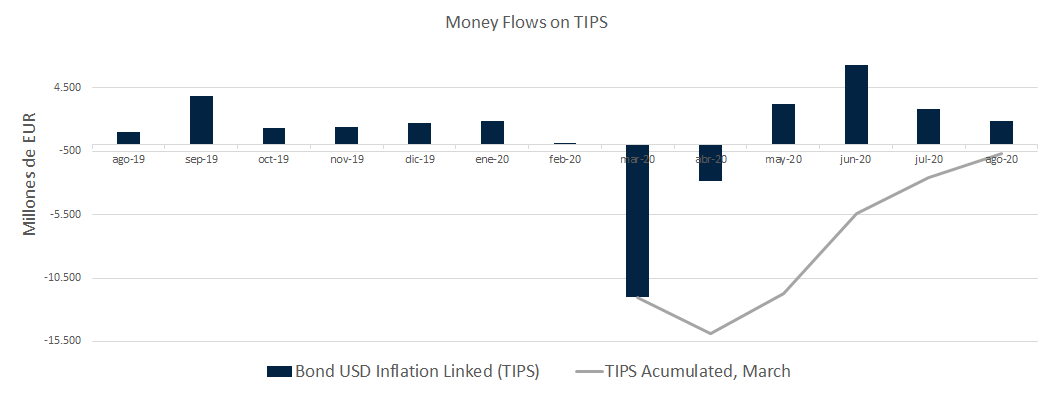

As a result of the Covid-19 crisis in March, investors came out on top of inflation-linked bonds (TIPS): they thought that when a forced crisis in demand arrived, deflation could occur that would harm the value of their investments in TIPS.

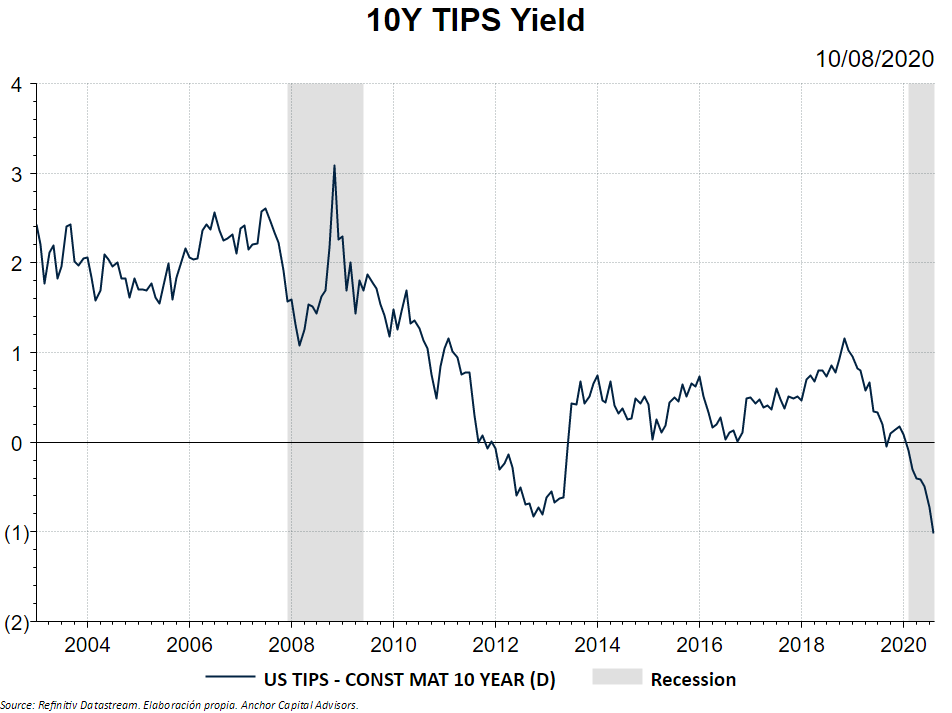

Recently, we are seeing how the real interest rates of the US economy are on negative ground.

In inflationary crises, the TIPS adjust to inflation and the interest rate they bear is attractive. On the other hand, in deflationary crises, the TIPS usually imply negative returns, since the principal and the coupon of the bond go down when the price level goes down.

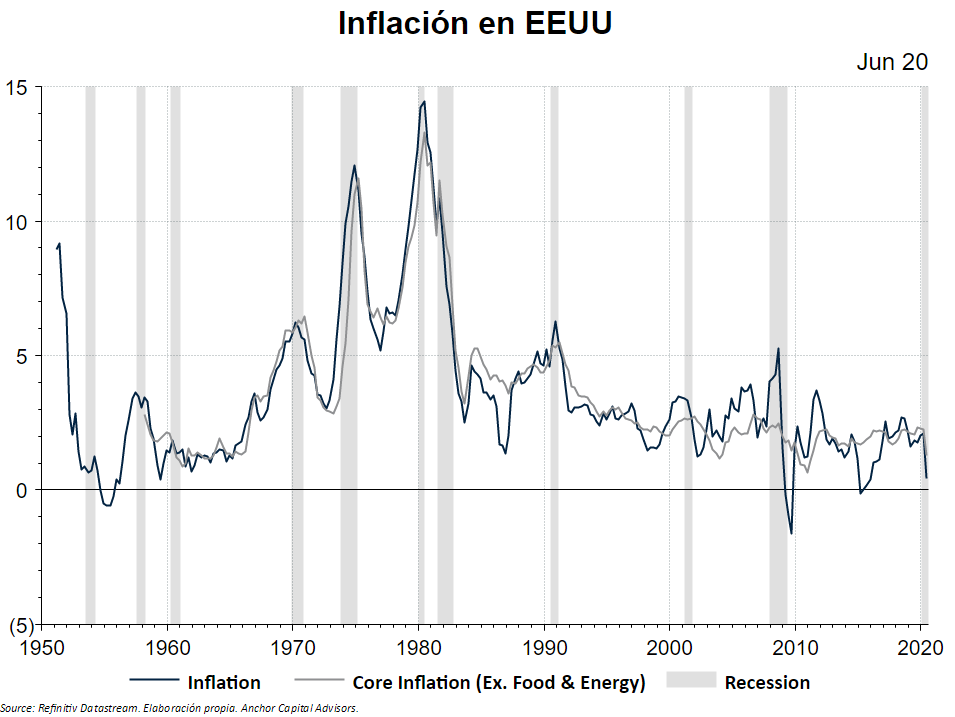

It is true that the Covid-19 crisis has all the elements for which we can think this is a deflationary crisis: a drop in demand, a significant contraction in GDP and a reduction in energy prices.

In addition, we must add other longer-term deflationary aspects such as the massive use of information and production technologies, globalization and the openness of economies.

Anyway, we witness that deflation did not arrive yet, among other reasons due to the aid packages approved by the US Congress and the Fed printing money massively.

What we are seeing is how, little by little, investors are regaining confidence in TIPS, despite having a negative return. The evidence is in the cash flows from May to today, where there has been a significant capital inflow .

Perhaps investors think there may be a rise in inflation, or they are simply diversifying their portfolio to cover all possible scenarios.

Anyway, it seems that this "bet" on inflation caused by the printing of Fed money is not working: the money is staying on Wall Street and citizen aid packages are only keeping demand and the price level. Certainly, high inflation would surprise many.