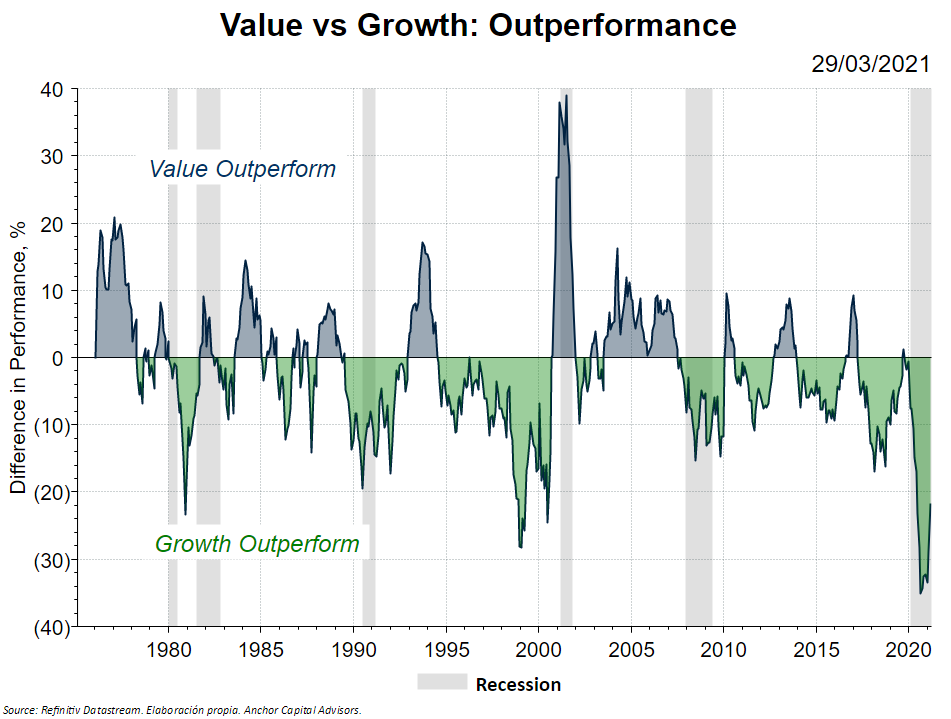

Over the past ten years we have become used to Growth stocks yielding much higher returns than Value stocks. So much so that never in history has Value Investing traded at such a discount compared to Growth.

This changed when the results of the vaccine clinical trials were published in November: since then, Value companies have outperformed Growth companies in terms of profitability.

However, as we see in the graph, there has been an historical balance between these two categories:

1Y S&P 500 Value - 1Y S&P 500 Returns. Reffinitiv Datastream. Elaboración Propia Anchor Capital Advisors.

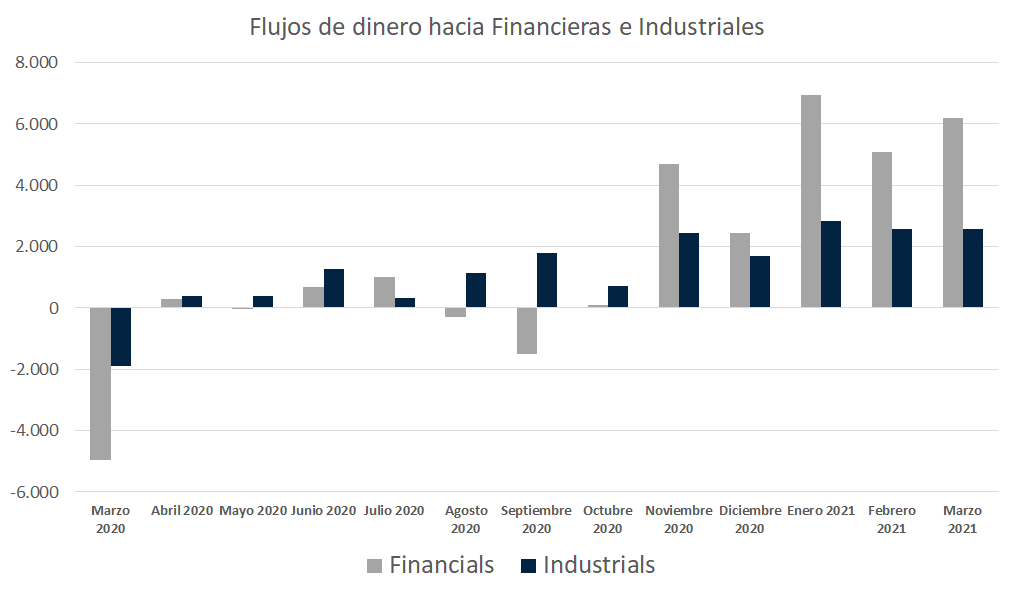

If we talk in terms of monetary flows, since November we have been seeing a clear rotation towards Industrial and Financial sectors. So far, we are not seeing clear signs that this rotation towards cyclical values will change in the short term.

In any case, it is important to mention that we have begun to see timid inflows of money in Consumer Staples and Utilities during this month of March, although we did not see inflows to other defensive assets such as gold.

Return to historical "normality"?

It may still be a bit early to ask that question, as the Value rally started in November. In any case, there would have to be a paradigm shift so that Value outperforms Growth for a long period of time, since the trend in recent years has been the opposite.

How long will the rally last?

"Until central banks want to" is a wild card answer to questions of this kind. In theory, in an environment of interest rate hikes, Value companies should do better than Growth companies.

In any case, in the period between 2015-2020 we saw rate hikes and Growth continued to outperform Value. As it often happens, the theory does not always conform to reality.