With the current economic data, what the macroeconomic textbooks suggest to us (sometimes a high-risk sport) is that we could be in a very late phase of the economic cycle.

A very fast economic cycle is what we could have seen with the recession caused by the pandemic: recession during the strictest lockdowns, recovery phase during the vaccination campaign and current overheating, with the full reopening of the economy.

On the contrary, some argue that the pandemic was simply hitting the off button on the economy, like a small power outage due to some technical problem in the network, easy to resolve. The problem is when the storm arrives and blows away the entire grid, and we cannot turn on the light for days. This would indicate the end of a longer cycle, which started during the past decade.

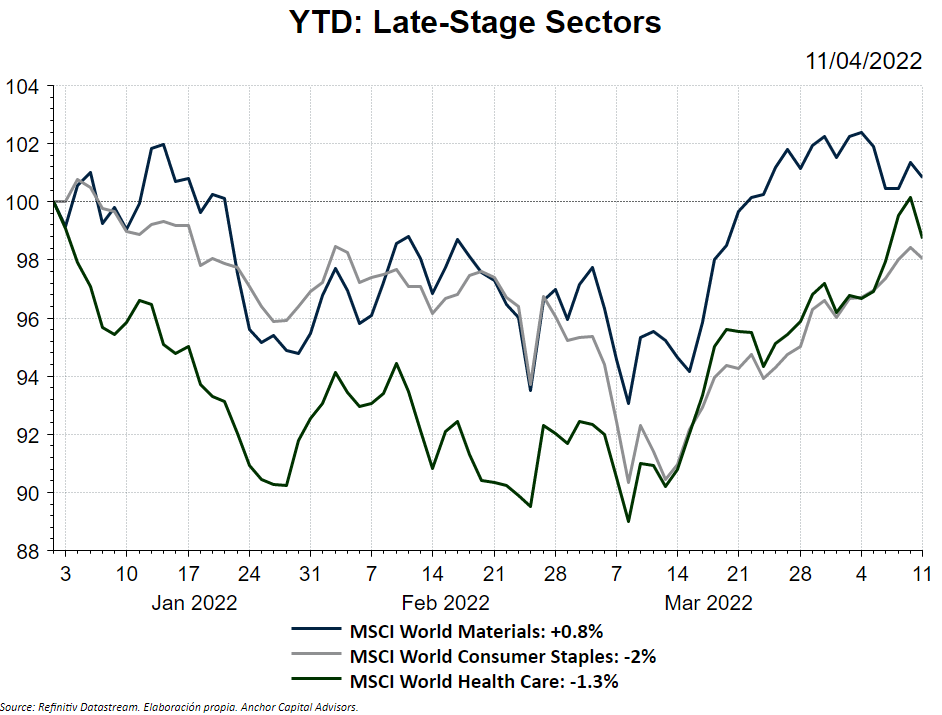

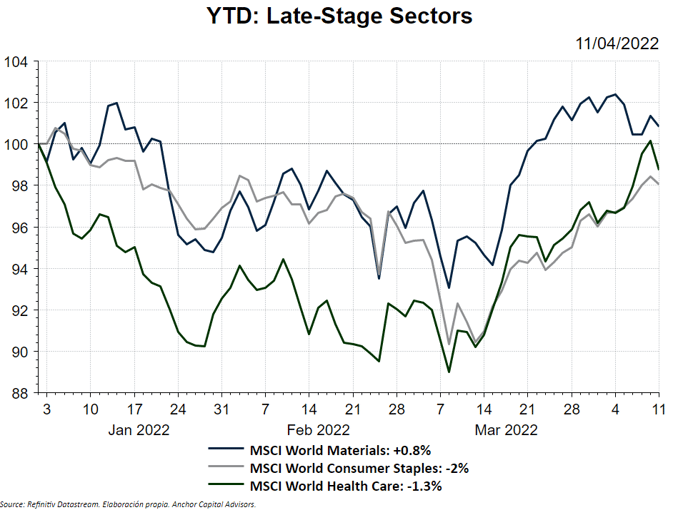

Which sectors tend to perform better in a late-stage cycle?

In any case, if we assume that thesis is correct, we can expect certain sectors to perform better on the stock market.

- Sealth: typically a more defensive sector. We can find high quality companies, resilient to possible crises.

- Consumer Staples: here we find many companies with great capacity to transfer cost increases to prices, especially those that offer a product whose demand is more inelastic.

- Energy and Materials: although it is already a bit late to jump on the Commodities bandwagon, we may still see price increases in the short term before demand slackens.

Where should we not be?

Everything that is cyclical, such as Consumer Discretionary, would seem to be quite affected. In addition, companies classified as Deep Growth, in a context of interest rate hikes, may lose a large part of their value on the stock market, so we would prioritize companies with present and not future cash flows.

In the coming months we will see if, once again, the macroeconomics textbook works or if it leaves us stranded in the middle of the road, as it has done more than once in the past.