The current socioeconomic context, triggered by the COVID 19 pandemic, has generated an unprecedented reaction from central banks worldwide.In an effort to contain the effects of the crisis, the US Federal Reserve has pursued an aggressive monetary policy, bringing interest rates to practically zero and expanding its balance sheet through asset purchase programs for more than 3 trillion dollars in just 4 months (after the 2008 crisis, the same amount was issued, but over the course of 6 years).

In addition to this, the FED has announced that it will apply a new approach to its monetary policy, where it will allow inflation to rise above 2% to compensate for previous falls. Taking into account that the FED has not hit the inflation target since 2012, and that even with a record unemployment rate of 3.5% in 2019, inflation didn't exceed the 1.6% threshold, the new Federal Reserve plan would invite to skepticism.

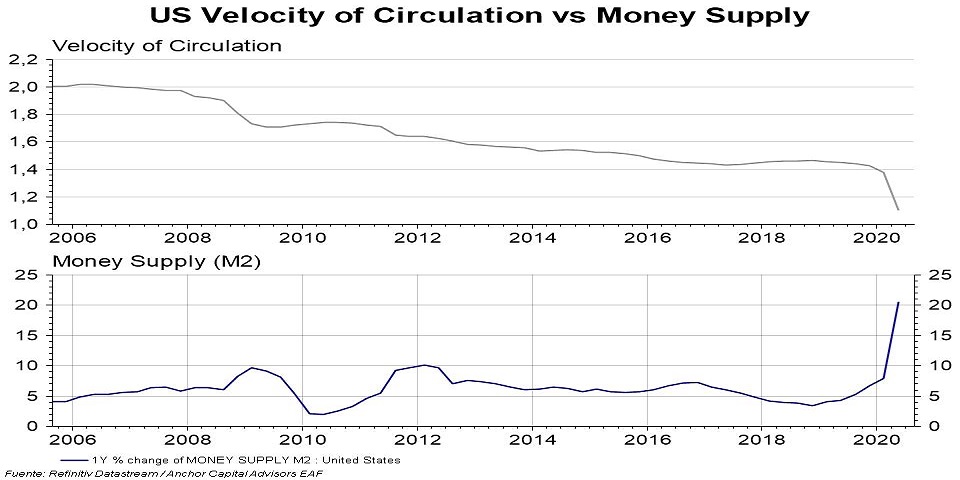

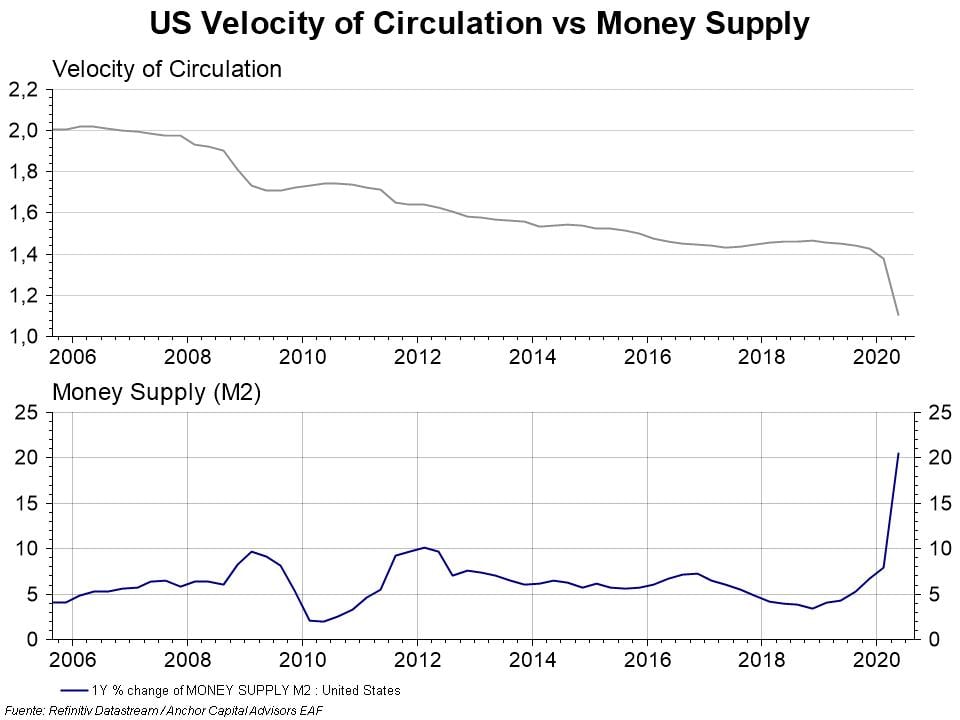

If we go to the data, in first place, the speed at which money circulates is increasingly slow, therefore, the slowdown in consumption would be taking precedence over monetary issuance and generating deflationary pressures. Second, the pandemic has left a lot of idle capacity in the economy and unemployment, two key factors in the formation of future prices.

The 2008 crisis has taught us that monetary issuance is not necessarily equivalent to inflation, since it depends on how it is transferred into the real economy. However, we must also consider that the current crisis has unprecedented fiscal intervention and indebtedness, and that international politics is making an exceptional effort to break the foundations that give credibility to central banks. Given this, the risks of inflationary pressures would seem more linked to a reduction in the reputation of the institutions than to changes in monetary policy.