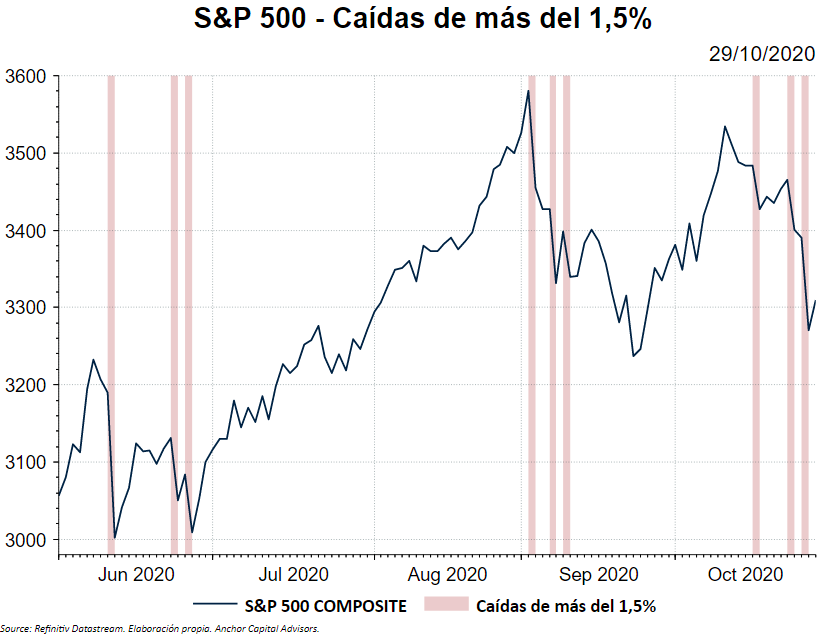

After a quiet summer vacation for the markets, back to school in September and the Halloween holiday are taking their toll.

Last week, the markets showed signs of more weakness: during the session on Wednesday October 28, the S&P 500 fell 3.53%.

This is one of the worst declines in the history of the index. In fact, this drop is within the 1% percentile of daily returns.

This means that only 1% of the days the S&P 500 has fallen 3.53% or more. It is easy to say it but hard to take on.

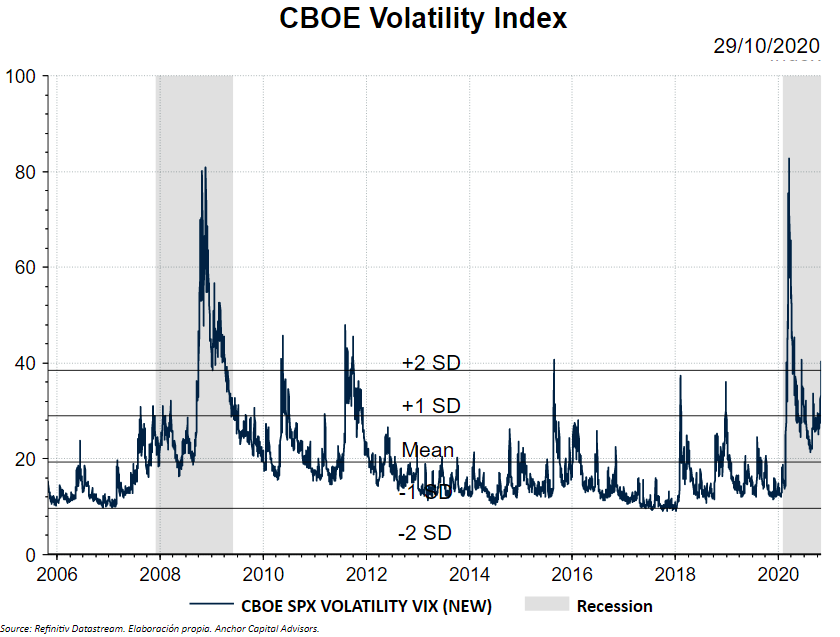

When will VIX return to "normal" levels?

Right now, we are at levels that exceed two standard deviations. This is concerning as it means that there is ongoing latent volatility.

The truth is that, as always, no one knows when this volatility situation will reverse. And it is that during the month of October came together the second wave of contagions in Europe and the lockdowns that this implies, the uncertainty of the American elections, earnings season results and, last but not least, a Brexit agreement that never comes.

Fortunately, companies earnings are being better than expected, which makes us more optimistic in this regard.

Perhaps the trigger to reassure the markets is a vaccine, but it seems that there are still a few months to make it possible. Everything points to volatility will last some more time.