The PE Ratio (Price to Earnings Ratio) is one of the most common when trying to determine if the stock market is expensive or cheap. However, it can give us the wrong signals if we do not understand it well.

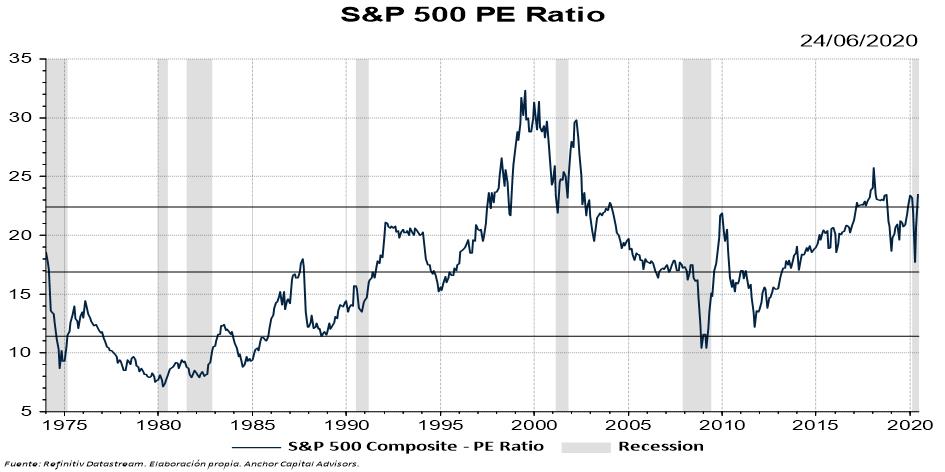

A little bit of history

As we can see, the value of the PE Ratio ratio has changed over time. The price of companies with respect to their profits is not always the same. That is because the market prices business profits based on expectations, which sometimes are not well set.

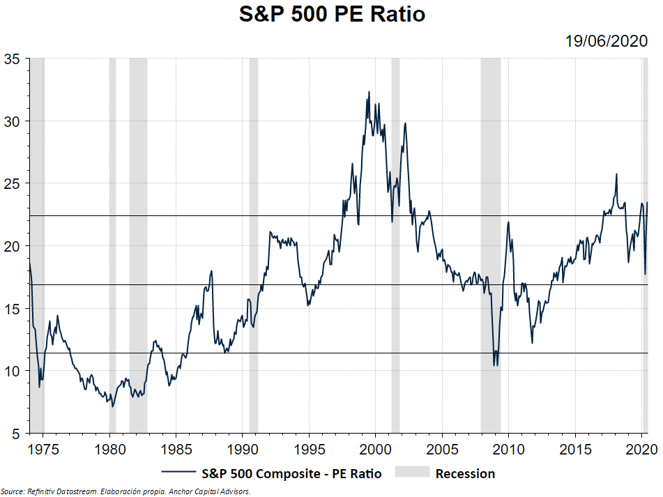

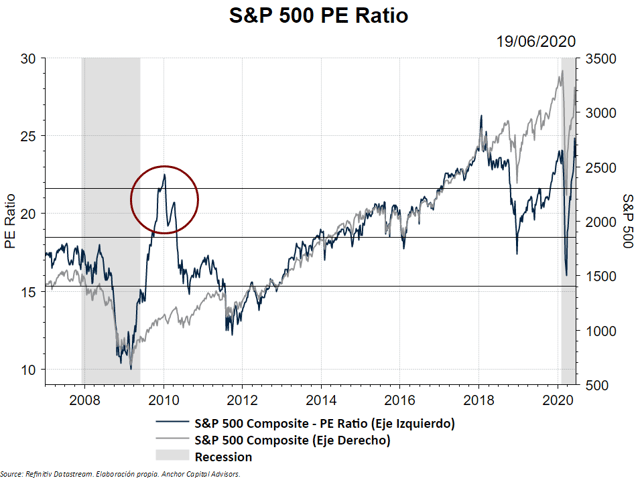

First Problem: Crisis and Profits drop

When corporate profits fall, the PE Ratio rises. This can be a problem, as the expectations of future benefits are not taken into account.

2010 would be a good example of that: profits fell sharply and the stock market seemed expensive (if we look at the PE Ratio), but it was not a bad year to invest.

One possible solution would be using the Forward PE Ratio, which takes into account the expected profits one year from now. But with this, what we are only doing is differing the problem: companies would look expensive one year from now.

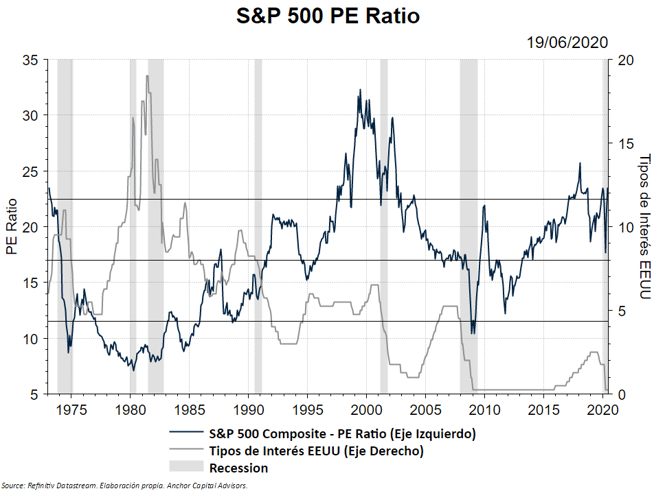

Second Problem: Interest Rates

One could think that the PE Ratio is independent from the interest rates. It's not usually like that.

If we think in terms of Cash Flows, logic tells us that a rise in interest rates automatically translates into a reduction in the present value of any future cash flow.

If we understand the future profits of companies as Cash Flows, then a reduction in the interest rates would imply an increase in the present value of those future profits.

In the chart we can see how when interest rates are low, the PE Ratio tends to be higher.

Therefore, in a low interest rate environment like the current one, we can expect the PE Ratio to be higher and, therefore, companies seem to be more expensive in terms of profits.

Despite these problems, the PE Ratio remains one of the fundamental metrics investors rely on to determine where to invest.

As we wrote a few months ago, corporate profits are the fundamental factor by which the price of a share moves in the long term.

Consequently, it is logic to think that a metric that incorporates corporate profits would be an important measure for investors.

In any case, one must know that no indicator is perfect. Understanding the setbacks of any measure is the key to use it well.