.jpg)

Although market consensus indicates that 2021 will be a positive year for equities, that does not mean that there are no risks. In this post, we will explain some of them.

Complications of Covid-19

Christmas holidays can have consequences in the form of infections and a third wave. This could mean a new total shutdown of the economy, especially at the beginning of the year, which is when the vaccine won't be available for everyone.

In the same way, a mutation of the virus could lead to the ineffectiveness of the vaccines. Without a doubt, this would be the worst case scenario.

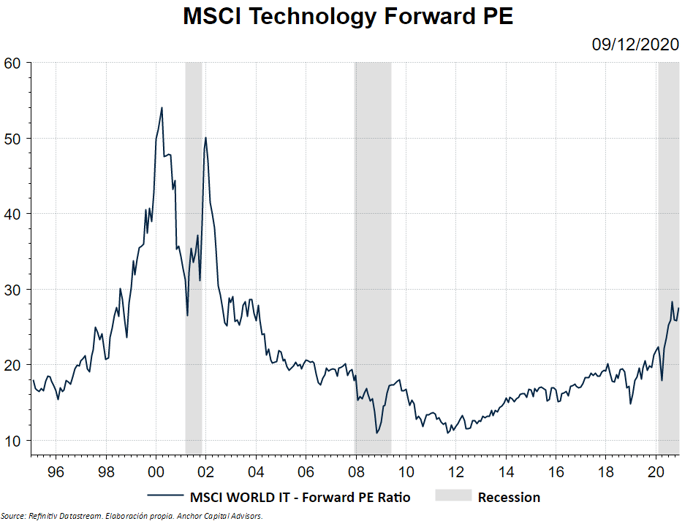

Technological crisis

Nasdaq is 42% YTD. If we look at the 5-year return, it is 167%. Another argument that supports the thesis that technology is too expensive are valuations, which are at the highest levels since the dot-com crisis.

Furthermore, even though the expected growth figure for the technology sector is 14% for 2021, it falls short when compared to the 22% expected EPS growth for the S&P 500.

Inflation

In the first place, the ultra-expansionary policies of the central banks, injecting liquidity at record figures, together with the expansionary fiscal policy and the recovery of the macroeconomic cycle, may suggest that there is a higher risk of inflation.

Another argument in favor of inflation could be deglobalization. The Covid-19 crisis has made it clear that global production chains carry certain risks, so it makes sense to think that both the United States and China will seek self-sufficiency in terms of production.

On the other hand, deflation could be another risk to take into account, but surely less probable one. Deflation as a consequence of poor macroeconomic figures may not be entirely good for risk assets.

However, a combination of high inflation and low growth would be perhaps the worst case scenario.

Defaults in China

Recently, we have seen companies that were theoretically backed by the Chinese government default.

This has hurt the local Chinese bond market. Despite that, if we look at the long term, it is good news for the market, as it rewards competition and wipes zombie companies.

However, an hypothetical lack of government support to many companies and a drain of liquidity in the market could lead to an outflow of capital and a contagion effect to other assets.

Debt crisis

One consecuence of a possible economic slowdown is a debt crisis, both in the US and in Europe. Debt ratios above 100% of GDP, despite low interest rates, pose a risk in the long term. Furthermore, low inflation does not help the indebted.

In any case, with Central Banks backing the markets, that it is unlikely that will happen, at least in the short term.

Politics and Geopolitics

The recent death of an Iranian scientist is an example of this type of risk, with geopolitical tensions in the Middle East as the focus.

At the same time, the risk of political disagreement between EU member countries is always present due to unanimous decision mechanisms and veto capacity.

What can we do to avoid them?

Beyond the obvious specific actions we can take to avoid these risks, such as divesting from technology or not buying Chinese or European bonds, the important thing is to be aware that there are always latent risks, and that their probability of manifesting increases when investors are euphoric.

Hopefully, during the year 2021, none of them will occur.

Another argument in favor of inflation could be deglobalization. The Covid-19 crisis has made it clear that global production chains carry certain risks, so it makes sense to think that both the United States and China will seek self-sufficiency in terms of production.

On the other hand, deflation could be another risk to take into account, but surely less probable one. Deflation as a consequence of poor macroeconomic figures may not be entirely good for risk assets.

However, a combination of high inflation and low growth would be perhaps the worst case scenario.

Defaults in China

Recently, we have seen companies that were theoretically backed by the Chinese government default.

This has hurt the local Chinese bond market. Despite that, if we look at the long term, it is good news for the market, as it rewards competition and wipes zombie companies.

However, an hypothetical lack of government support to many companies and a drain of liquidity in the market could lead to an outflow of capital and a contagion effect to other assets.

Debt crisis

One consecuence of a possible economic slowdown is a debt crisis, both in the US and in Europe. Debt ratios above 100% of GDP, despite low interest rates, pose a risk in the long term. Furthermore, low inflation does not help the indebted.

In any case, with Central Banks backing the markets, that it is unlikely that will happen, at least in the short term.

Politics and Geopolitics

The recent death of an Iranian scientist is an example of this type of risk, with geopolitical tensions in the Middle East as the focus.

At the same time, the risk of political disagreement between EU member countries is always present due to unanimous decision mechanisms and veto capacity.

What can we do to avoid them?

Beyond the obvious specific actions we can take to avoid these risks, such as divesting from technology or not buying Chinese or European bonds, the important thing is to be aware that there are always latent risks, and that their probability of manifesting increases when investors are euphoric.

Hopefully, during the year 2021, none of them will occur.