Fixed Income has not been spared from the terrifying consequences of the recent war. The tension has also taken hold of the markets, where we have seen increases in the price of CDS (Credit Default Swaps, insurance against non-payment) of many sovereign countries.

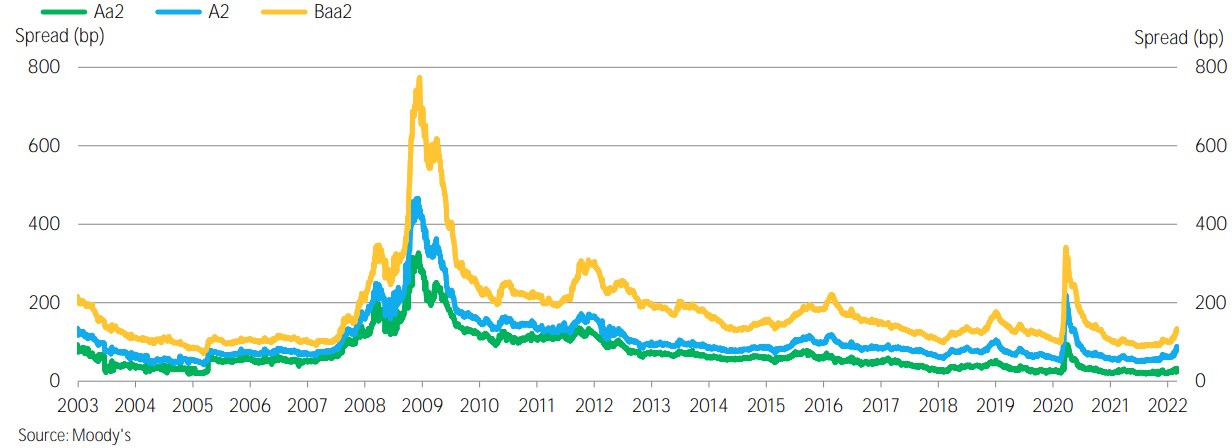

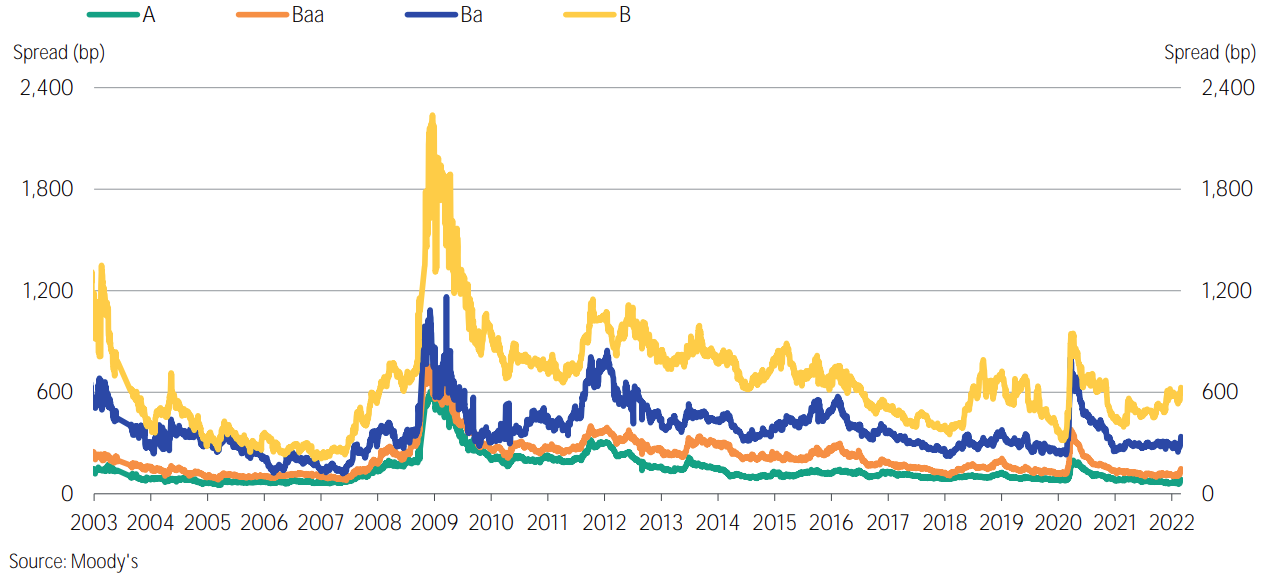

At the same time, we have also seen consequences in corporates, both in EUR and USD, in the form of widening spreads and higher yields.

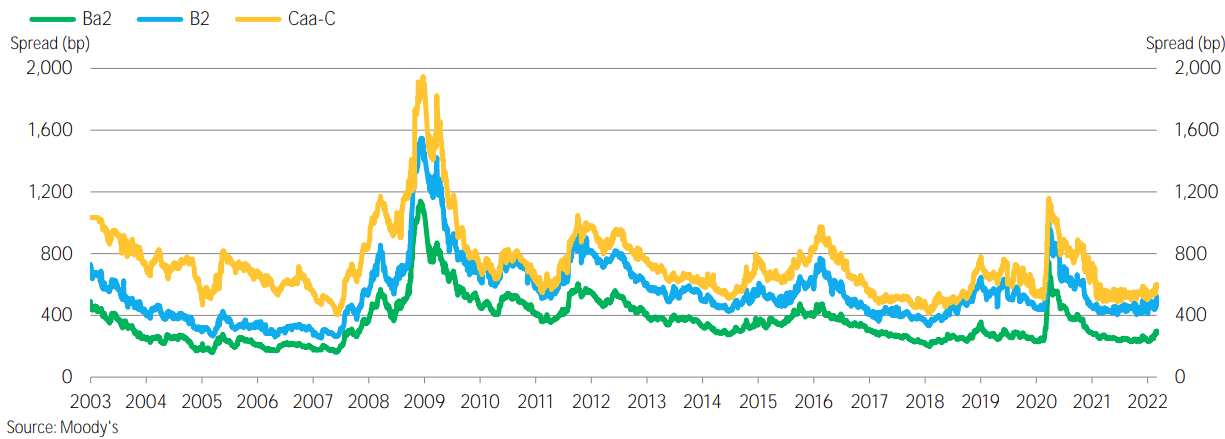

In High Yield, we are also experiencing a substantial increase in yields and, as a consequence, price falls close to 5%, evaporating the gains of the previous year.

In the Emerging Markets, the story is very similar. However, we do see more signs of stress in the High Yield spectrum, where we see that spreads have increased more than in other ratings.

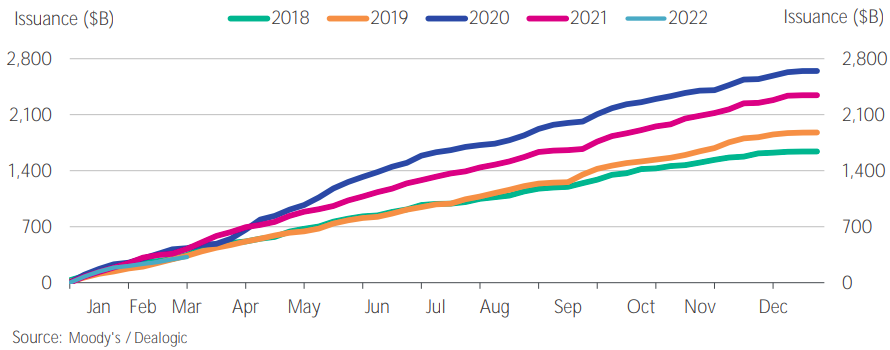

At the same time, with the rate hikes and the withdrawal of stimulus, we are seeing that liquidity is shrinking. A direct consequence of this is the decrease in new debt issues by companies in the primary market. As we can see in the graph, the trend for this 2022 is clearly downward.

Probably, during this 2022 we will neither reach the levels of 2020, where companies issued debt to finance the problems arising from the covid crisis, nor those of 2021, where rates were still low.

Unlike in the Equity space, Fixed Income, in the absence of defaults, offers a yield already known at maturity. With these increases in yields, we can say that Fixed Income is more attractive now than before.

In any case, it is possible that, along the way, we will have to assume more volatility (besides from the geopolitical tensions, we must add the withdrawal of liquidity from central banks and the rate hikes).

In conclusion, we see good entry points with Investment Grade spreads on 150-200 basis points and High Yield spreads above 450-500. As long as we hold securities to maturity, we will have higher yields than we did a couple of months ago.