Bad inflation data is leading the Fed to act faster than initially expected. The large amount of monetary and fiscal stimulus in the wake of the covid crisis, as well as the rise in energy prices and supply problems are leading to the highest inflation since the 1970s.

With this on the table, one would tend to think is that the categories with the longest duration, such as equities and very long-term fixed income, would suffer more in a context of rate hikes. Well, are these the assets that have suffered the most?

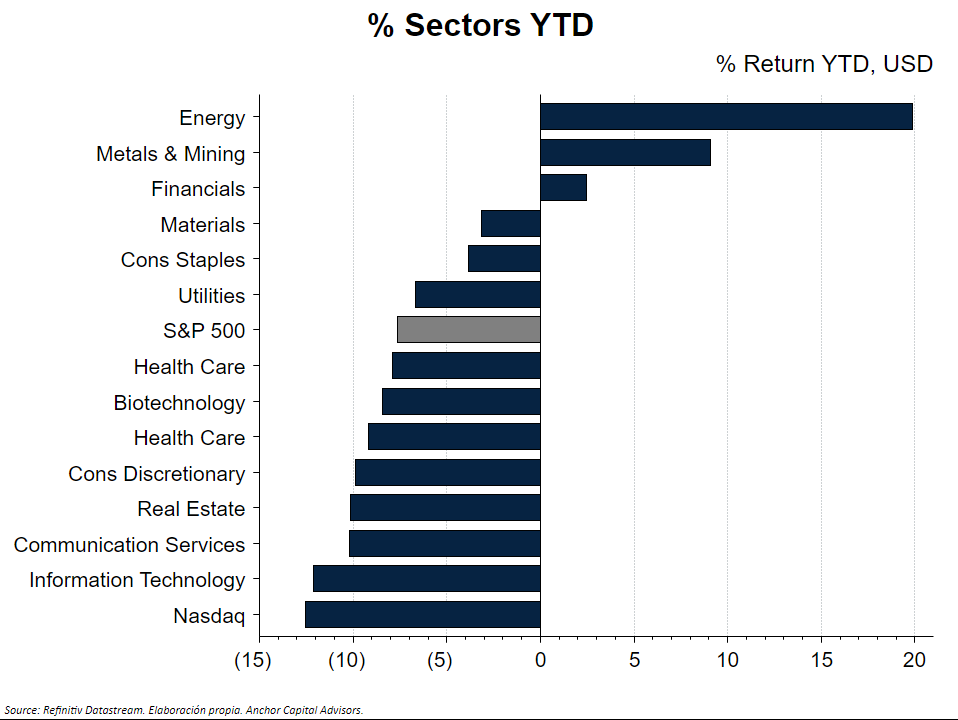

Well, the answer is halfway. As we see in the graph, the Growth has suffered more this beginning of the year:

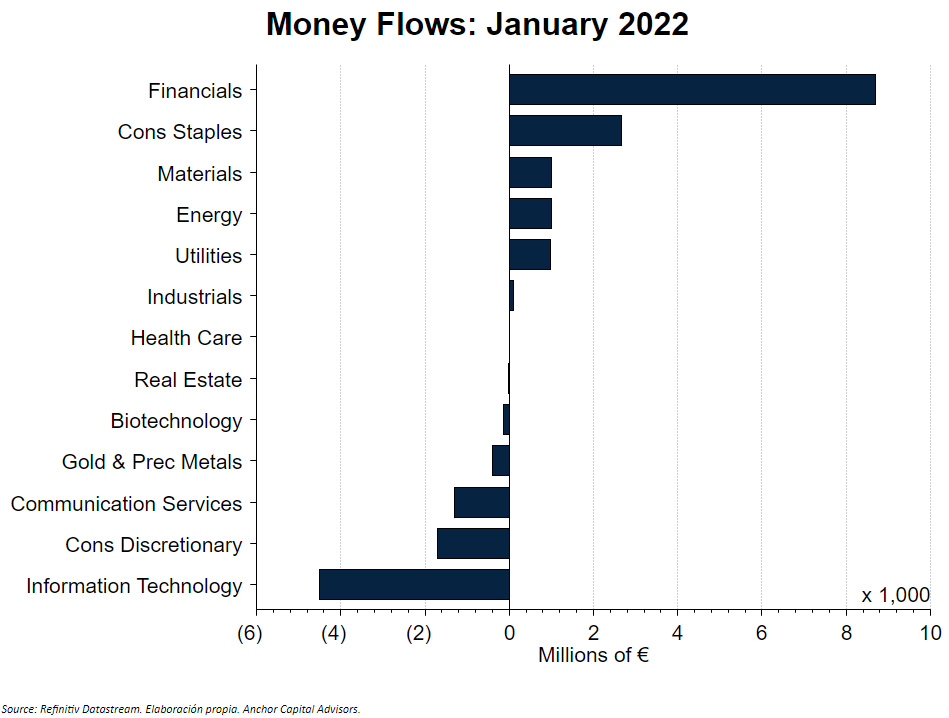

If we look at the money flows, we see how investors have not taken refuge in fixed income assets, but have chosen to rotate their technology portfolio towards more defensive sectors, such as Consumer Staples or Utilities. Furthermore, they have opted for Financials (apparently benefited in a context of rate hikes) and Energy.

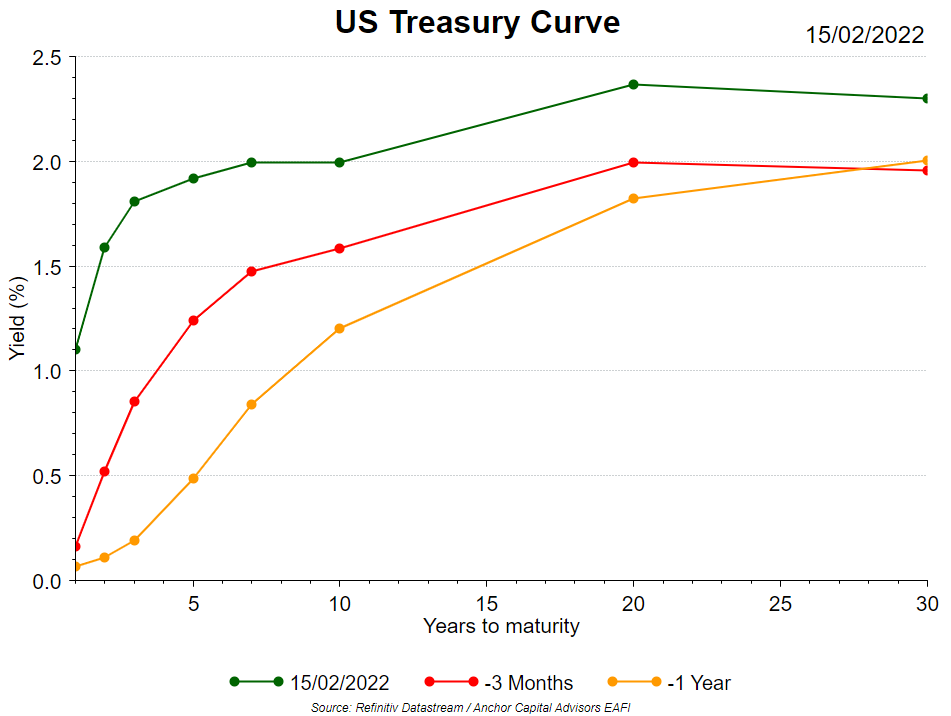

The increase in correlation has also taken its toll: rate hikes are causing the curve to move up, especially the short legs.

Here, short-term fixed income investors also suffered, and the asset did not fully serve as a safe haven from stock market declines as it also fell in value.

In conclusion, it seems that this Fly to Quality is taking place more at a sector level within the Equity category and in more tactical bets such as Financials or Utilities. Investors fear that rate hikes will affect them, whether in shorter or longer periods, so they choose to rotate their portfolio towards sectors with better dividends, prioritizing current cash over future cash in a long-lived asset. Will they succeed this time?