In portfolio management, diversification is efficient when correlations between assets are low.

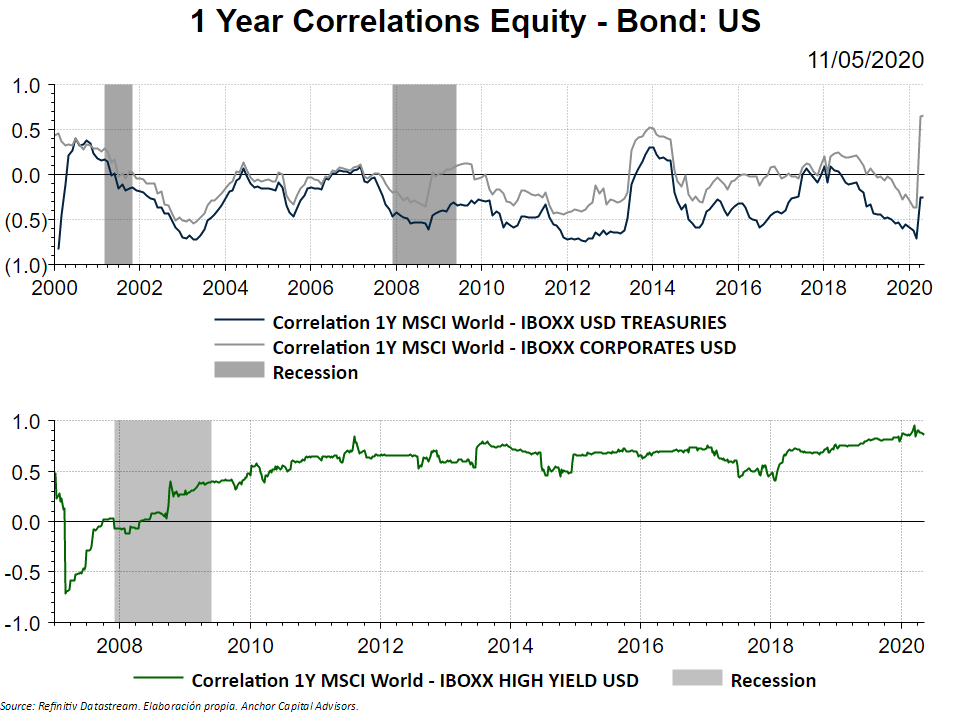

In the last Great Financial Crisis, the correlations between bonds and equities remained more or less stable. However, during the Covid-19 crisis they are reaching higher levels.

However, the negative correlation remained in American government bonds, but we have also seen a little rebound.

The 10-year US bond hit record lows last month as global stock markets plummeted. In this sense, this was positive for some investors that had previously invested in the safe haven.

This was not the case of the Investment Grade Corporate Fixed Income, which suffered a large upturn in the correlation: when the Equity market fell, the prices of the bonds issued by the companies also did.

Since the virus crisis was generated in a few months and the shock was fast, the market discounted these negative variables at the same time. At the end of the day, the shareholder and the bondholder have shared interests: company must do well in order to get their payments, either dividends or interest.

On the other hand, historically, the High Yield has never been a source of de-correlation with Equities. In fact, this type of asset is more similar, in terms of behavior, to Equity than to Fixed Income.

One of the big questions we ask ourselves is whether the correlations will remain high in the long term. These will surely experience a decrease in the short term, but it is possible that in the medium and long term they will remain in higher ranges than the historical average.

In conclusion, we can say that the correlation can disappoint us when we need it most. This is certainly a key factor when building portfolios.